Settle Insurance Claims in Days, Not Months

Reducing Fraud With Drone, ROV & Digital Twins.

Increasing Clarity. Accelerating Decisions By Building Confidence

Your policyholders are waiting. Your adjusters are backlogged. Your fraud exposure is growing. Drone & Robotic Inspections, reducing your backlog by by up to 60%.

The Market Has Shifted. With $58.9b In Claims paid in 2025 & $2.2b in estimated fraud. Has Your Approach Changed Too?

CASA Certified

|

ISO 9001

ISO 45001

ISO 14001

Aligned

|

$20M Public Liability

|

CASA Certified | ISO 9001 ISO 45001 ISO 14001 Aligned | $20M Public Liability |

Paying the Compounding Cost of Slow & Subjective Assessments

Volume:

$4.8 billion in insured losses from 294,000 claims during 2025 alone, driven by extreme weather events, which are increasing in both frequency and severity. Ex-Tropical Cyclone Alfred generated 132,000 claims in a single event. Your field assessors cannot physically reach every property fast enough.

$4.8B | 294,000 claims | 5 declared catastrophes in 2025 alone (ICA, 2026)

Process:

Your current process has structural weaknesses. Ground-based adjusters face safety risks on damaged structures. Flood-affected areas are inaccessible for days. Manual inspections are subjective, inconsistent, and slow. Every day of delay compounds policyholder distress, increases operational cost, and exposes you to complaints and regulatory scrutiny.

2-4hrs | Per traditional property assessment, including travel

Fraud:

$2.2 billion is estimated to be lost to fraudulent claims annually. Without objective, timestamped, high-resolution evidence captured at the point of loss, your fraud detection relies on subjective information. Only $560 million was detected as opportunistic fraud in 2023 alone; undetected fraud is estimated to be almost 75% higher.

$2.2B | Annual fraudulent claims (IFBA)

For litigation firms needing court-admissible forensic evidence, see Legal & Litigation Support.

If your adjusters visit one property at a time:

After a major event, the queue stretches for weeks. Every day compounds policyholder distress, increases operational cost, and exposes you to complaints. At 2-4 hours per traditional assessment, including travel, a backlog of 294,000 claims is impossible.

If you rely on desk-based aerial imagery (Nearmap, EagleView, satellite):

Your imagery is weeks or months old by the time of the claim. Top-down only. 5-7cm resolution cannot identify membrane failures, measure crack width, solar panel damage, or detect moisture ingress. When a cyclone hits, you wait for its next scheduled capture. You cannot produce evidence that holds up in disputed claims.

If you have tried an in-house drone program:

You are carrying fixed costs for variable demand that changes rapidly. Two pilots cannot become twenty during a CAT event. Your technology freezes at whatever you purchased. When you need advanced sensors, thermal, underwater, confined space, or ground-level 360 capture, and the capabilities to analyse and report, you are back to outsourcing. You are managing aviation regulatory compliance, pilot currency, and digital twin creation, and processing and analysing data as an insurer, not as a technology company.

Results at Scale

30%

Reduction in loss adjustment expense

$100,000+

Saved per estimator per year

37%

Faster Claims Settlement

60%

Reduction in inspection backlogs during peak disaster

Built for Insurance Professionals Who Need Better Evidence, Faster

Whether you are managing claims, pricing risk, investigating fraud, or responding to catastrophe events

Claims Directors & Loss Adjusting Managers

Backlogged assessments, rising LAE, policyholder complaints escalating during CAT events. Your team cannot physically reach every property fast enough, and every day of delay compounds cost.

Underwriting & Risk Managers

Pricing premiums on assumptions, not data. No property-level condition intelligence. Reinsurers demanding better data. Drive-by photos and Google Street View are not evidence.

CAT Response & Surge Operations

Fixed team cannot scale. Two pilots cannot become twenty. Procurement takes weeks when disaster strikes. 132,000 claims from a single cyclone overwhelms any internal capacity.

Fraud & Special Investigations

$2.2 billion lost to fraudulent claims annually. 75% goes undetected. No pre-loss baseline. Relying on adjuster judgment and inconsistent documentation that cannot withstand scrutiny.

Property & Strata Portfolio Managers

Managing hundreds of properties with no standardised condition data. Maintenance decisions based on complaints, not evidence. Capital works budgets based on estimates, not measurements.

Subrogation & Recovery Teams

Proving third-party liability requires evidence that the damage was caused by their negligence, not pre-existing conditions. Without objective before-and-after documentation, recovery claims are contested and abandoned.

What Your Claims Operation Looks Like With a Structured Capture Program

37%

Faster Claims Settlement

500%

Productivity Improvement for Remote Adjusters

400%

Faster Claims Estimation

30%

Reduction in Loss Adjustment Expense

After a catastrophic event, the entire affected area can be captured within 48 hours. Your desk-based adjusters remotely navigate to any property in the dataset, measure damage, and complete assessments. One mobilisation covering hundreds of properties. Pre-loss baselines already exist for your high-value portfolios. Evidence is measurement-grade, timestamped, and holds up in any dispute.

Traditional Assessment vs. Structured Intelligence Program

A managed inspection program does not just reduce cost. It creates intelligence infrastructure that compounds in value across routine operations and catastrophe response alike.

Traditional (Reactive)

One property. One visit. One report. No cumulative value. Same cost whether routine or urgent.

Structured Program (Capture)

Scheduled captures for BAU. Surge capacity for CAT. Standardised data builds portfolio intelligence over time.

Platform Intelligence (Digital Twin)

AI-powered. Portfolio-wide. Predictive. Routine monitoring prevents claims. Event response is instant because the baseline already exists.

Assessment Cost

Traditional

$500 - $1,500+ per property. Adjuster travel, time on-site, admin overhead. Same cost whether it is a routine renewal inspection or a post-event claim.

Structured

From $250 per property. Batch capture, processing, condition report, platform delivery. Volume pricing at program scale reduces cost further for annual portfolios.

Platform

Decreases over time. Subsequent captures are faster because the baseline already exists. Routine annual captures cost less each cycle. Post-event assessment is near-instant because only change needs evaluation.

Assessment Speed

Traditional

Days to weeks. Schedule adjuster, travel, wait for report. One property at a time. Routine renewal inspections compete for the same limited field capacity as claims.

Structured

Routine: Scheduled captures aligned to renewal cycles, completed in predictable timeframes. Event: Same-day to 48hrs batch capture of entire affected zones. Reports within days either way.

Platform

Routine: Automated change detection flags deterioration between scheduled captures. Event: Pre/post overlay available the moment post-event data is uploaded. AI flags changes automatically. No waiting for a human to compare.

Scalability & Program Flexibility

Traditional

Fixed capacity regardless of demand. Routine inspections backlog when claims spike. CAT events create 1-4 week queues. Overtime rates. Adjuster burnout. No flex between BAU and surge.

Structured

BAU: 5 properties this month, 50 next quarter — scales to your renewal schedule without fixed headcount. CAT: Same infrastructure pivots to area-wide response within 24-48hrs. No idle capacity cost between events.

Platform

Force multiplier in both modes. Routine: One scheduled capture serves underwriting, claims, and portfolio management teams simultaneously. Event: One capture serves unlimited desk adjusters. Portfolio-wide triage from a single dataset regardless of whether it is BAU or disaster.

Data Consistency

Traditional

Varies by adjuster. Handheld photos, inconsistent angles, no measurements. Quality depends on individual. Routine inspections and claims assessments produce incomparable data.

Structured

Standardised. Calibrated sensors, consistent methodology, georeferenced, measurement-grade. Every property captured the same way whether it is a routine annual baseline or a post-event assessment. Data is directly comparable year-over-year.

Platform

Machine-readable. AI defect detection (cracks, spalls, roof condition). Automated condition scoring. Quantified measurements, not subjective opinion. Consistent grading across your entire portfolio enables benchmarking and trend analysis.

Fraud & Dispute Prevention

Traditional

Reactive. No pre-loss baseline. Relies on adjuster judgment. 75% of fraud goes undetected (IFBA). Routine inspections produce no evidence usable in future disputes.

Structured

Proactive. Routine annual captures create the pre-loss baseline automatically. When a claim is lodged, post-event comparison shows exactly what changed and when. The baseline you built during BAU becomes your strongest evidence during a dispute.

Platform

Evidence-grade. Measurement overlay quantifies damage. Metadata integrity (GPS, time, calibration). Eliminates ambiguity that fraud relies on. AI flags discrepancies between pre-loss and post-loss automatically. Routine monitoring makes fraud nearly impossible to sustain.

WHS Exposure

Traditional

High — in both routine and emergency scenarios. Routine roof inspections still require height access, edge protection, and harness systems. Post-event: personnel on damaged roofs, in flood zones, near structural collapse. Premium workers comp costs regardless of whether it is BAU or CAT.

Structured

Eliminated. Remote capture for routine renewals and post-event assessment alike. No personnel on roofs, damaged structures, or in confined spaces. Zero height-at-work exposure whether you are capturing an annual baseline or documenting cyclone damage.

Platform

Documented. Platform records all access decisions and methodology. Audit trail for WHS compliance across routine and emergency operations. Evidence for subrogation if third-party negligence caused the damage. Your duty of care is demonstrably met.

Portfolio Visibility

Traditional

None. Individual claim files in separate systems. No aggregate view. No predictive capability. Routine inspections produce isolated reports that never connect to portfolio strategy.

Structured

Asset-level. Each property has a condition record updated with every scheduled capture. Searchable, measurable, comparable. Your routine program builds the portfolio intelligence that informs renewal decisions and capital planning.

Platform

Portfolio-wide intelligence. Deterioration tracking across all assets over time. Risk concentration mapping. Renewal pricing informed by actual condition data, not postcode averages. Predictive maintenance triggers alert you before a claim occurs.

Underwriting Support

Traditional

Limited. Drive-by photos or Google Street View. No interior, no thermal, no measurement. Underwriters price risk on assumptions because objective property data does not exist at the point of policy issuance.

Structured

Comprehensive. Aerial, thermal, interior 360, facade. Full property envelope captured before policy issuance as part of your routine underwriting workflow. Condition data available at the point of risk decision.

Platform

Risk-priced. AI condition scoring informs premium calculation. Thermal identifies hidden risks (moisture, electrical) before they become claims. Objective data replaces assumptions. Annual recapture tracks whether the insured is maintaining the property to the standard you priced for.

Recurring Value

Traditional

Zero. Each assessment is a one-off cost. No cumulative benefit. No learning. Last year's inspection report has no connection to this year's. You start from scratch every time.

Structured

Builds over time. Annual captures create a condition history. Each year's data is more valuable than the last because it enables comparison. Your routine program creates the evidence base that protects you during disputes years later.

Platform

Compounding intelligence. Multi-year deterioration models predict which properties will generate claims. Routine monitoring prevents losses before they occur. Claims forecasting from actual asset behaviour, not actuarial tables alone. The longer you run the program, the more valuable it becomes.

Estimate Your Program Savings

Enter your portfolio details to see the annual value of a structured inspection program versus reactive, one-off assessments.

Value Breakdown

Platform Intelligence Value (Not Quantified Above)

These estimates are conservative. They do not include speed-to-settlement value, reduced complaints, or reinsurer premium benefits from improved data quality.

Scope Your Program → Call Direct: 0492 449 655Three Ways to Start. One Path to Continuous Program.

Service Tier 1: On-Demand Assessment

For: Individual property claims, underwriting inspections, and dispute evidence

Your adjuster needs evidence for a specific property. A single mobilisation captures the complete condition record across all environments the property requires: roof, facade, surrounds, interior, and substructure. Sub-centimetre resolution. Georeferenced. Timestamped. Delivered within 5 business days.

Pricing indicator: From $250 per property (image capture, batch assessment). Condition reports and 3D models priced on scope.

What You Receive

Sub-centimetre imagery across all angles (not just top-down)

Thermal overlay identifying hidden moisture and leak paths

Georeferenced, timestamped evidence package with chain of custody

Optional interactive 3D model with measurement tools

Delivered within 5 business days of capture

What It Replaces

Weeks of individual site visits across the zone

Queue of 200+ properties waiting for one assessor

Dispute about what was pre-existing damage

Fixed team that cannot surge beyond its headcount

Service Tier 2: Area-Wide Catastrophe Capture

For: Post-disaster or large scale batch assessment, CAT event response, multi-property claims

With 132,000 claims from a single cyclone, your adjusters cannot physically reach every property. An area-wide capture documents the entire affected zone as a single georeferenced dataset. Multiple desk-based adjusters then navigate the interactive model to their assigned properties and complete assessments remotely from their desks within 48 hours of capture.

What You Receive

The entire affected area captured in one mobilisation

Every property accessible remotely by multiple adjusters simultaneously

Pre/post comparison if an annual baseline exists

Scalable to any event size (network scales, your payroll does not)

Browser-based platform access for your team (no software install)

What It Replaces

Relying on policy inception photos (often years old)

Manual comparison of outdated records

Reactive claims processing after failure

Property-by-property assumptions and conservative pricing

Siloed data in individual claim files

Procurement delay when disaster strikes

Why this matters commercially: You pay for one capture. You get remote assessment capability for every property in the zone. Your cost per assessment drops. Your speed increases. Your adjusters handle 3x more claims per day without needing to travel or leaving their desks.

Priority mobilisation slots are limited during peak season. Program clients receive guaranteed response within 24-48 hours.

Service Tier 3: Annual Baseline Program

For: Portfolio risk management, renewal underwriting, fraud prevention, reinsurer data requirements

When a claim arrives, the question is always: "Was this damage pre-existing?" Without a baseline, that question relies on subjective judgment. An annual capture program means the pre-loss evidence already exists. No dispute. No delay. No fraud opportunity.

Your reinsurer wants property-level condition data for renewal pricing. Your underwriting team needs current condition intelligence, not assumptions. An annual program delivers both while simultaneously building the fraud-proof evidence base that eliminates disputes.

Pricing model: Annual program, priced per property per capture cycle. Volume pricing applies. Retainer includes priority CAT response guarantee.

What You Receive

Annual condition capture of high-value/high-risk properties, even prior to policy approvals

Automated change detection between annual captures

Deterioration is identified before it becomes a claim

Portfolio-wide condition scoring for reinsurer reporting

Interactive digital twin platform for underwriting and claims teams

Digital Surface Models and thermal overlays, detecting defects before they’re visible

Priority CAT response mobilisation (retainer benefit)

What It Replaces

Adjuster climbing a damaged roof with a clipboard |

Guesswork about concealed damage |

Subjective photos on a phone with no metadata

Tape measure and estimation

2-4 week traditional assessment timeline

Why this matters commercially: The insurer who has pre-loss baselines settles claims faster, detects fraud earlier, prices premiums more accurately, satisfies reinsurer data requirements, and identifies deterioration before it becomes a loss. This is the shift from reactive claims processing to proactive portfolio intelligence.

| Property Type | Insurance Use Case | Why This Matters Now | How We Capture It | Digital Twin & Platform Value |

|---|---|---|---|---|

| Residential (Batch) | Post-CAT roof assessment, hail damage, storm claims | 294,000 claims in 2025. In the US, 68% of large insurers use drones for CAT claims. | Aerial batch capture, orthomosaic | Multiple adjusters assess properties simultaneously from their desks. Pre/post overlay comparison eliminates disputes about pre-existing damage. Measurement-grade evidence replaces subjective phone photos. |

| High-Rise / Strata | Facade condition, balcony defects, pre-policy baseline, renewal inspections | Saves 40-60% vs scaffolding. In the US, 57% of commercial property insurers use aerial inspections for underwriting. | Aerial + confined space (balconies, plant rooms) | Interactive 3D model lets underwriters navigate every facade, balcony, and plant room without site access. Automated change detection between annual captures identifies deterioration before it becomes a claim. Feeds directly into iTwin for portfolio-wide condition scoring. |

| Commercial | Roof condition for underwriting, renewal inspections, loss control pre-visits | Inspect roofs 6 months before policy renewal to adjust premiums. Ongoing program structure. | Aerial + thermal | Thermal overlay within the digital twin pinpoints moisture ingress and membrane failures invisible to visual inspection. Condition data feeds premium adjustment decisions with objective evidence rather than assumptions. Historical captures create a deterioration timeline for renewal pricing. |

| Industrial | Risk assessment before policy issuance, post-incident documentation, subrogation evidence | High-value assets, complex structures, hazardous environments. In the US, 57% use aerial inspections. | Aerial + thermal + confined space + ROV | Multi-environment data fused into a single navigable model via iTwin. Engineers and adjusters measure structural elements remotely. Subrogation evidence is timestamped and georeferenced with full chain of custody. Complex assets documented once, accessed by multiple stakeholders indefinitely. |

| Agricultural / Rural | Crop damage, flood extent, fire damage, livestock loss | Large area coverage needed. Orthomosaic mapping of entire properties. | Aerial large-area mapping | Georeferenced orthomosaic quantifies exact hectares affected. Overlay against pre-loss baseline proves extent of damage versus pre-existing conditions. Area calculations are precise and defensible, replacing manual estimation and disputed boundaries. |

| Recreational | Structural compliance, ride inspection support, post-event damage | High-value niche. Theme parks, resorts, and sporting facilities need facade and structural condition for renewal. | Aerial + confined space | High-value, complex structures documented in full 3D for renewal underwriting. Condition trends tracked across capture cycles to identify maintenance failures that could trigger future claims. Supports compliance evidence requirements without repeated physical access. |

| Marine / Waterfront | Hull inspection, marina damage, port infrastructure, flood damage below waterline | Flood events damage submerged infrastructure. Marine claims require underwater evidence. | ROV + aerial | Above and below waterline data fused into a unified digital twin. Adjusters inspect submerged damage remotely without dive teams. Corrosion mapping and hull condition tracked over time for marine underwriting. Evidence package covers the full asset regardless of access constraints. |

| Land / Broadacre | Flood extent mapping, erosion, subsidence, boundary disputes | Post-flood claims need georeferenced evidence of water extent and damage area. | Aerial large-area orthomosaic + LiDAR | LiDAR-derived Digital Surface Models quantify erosion volume and subsidence with centimetre precision. Flood extent mapped against cadastral boundaries for unambiguous coverage determination. Pre/post terrain comparison proves ground movement that visual imagery alone cannot capture. |

One Provider. Every Environment.

Measurement Grade Outputs. Enterprise Platform.

The reason most drone inspection experiences fall short is not the drone. It is the gap between image capture, processing, analysis, decision support and actionable intelligence. A local operator can fly. But can they process photogrammetry to sub-centimetre, interactive inspection accuracy? Deliver an interactive digital twin that your adjusters can navigate from their browsers? Detect moisture through radiometric thermal analysis? Capture submerged infrastructure with an underwater ROV? Scale from 3 properties to 300?

The combination is what changes your operation:

Multi-environment: Aerial, high-resolution visual, radiometric thermal, ground-based 360 ° visual, LiDAR and thermal cameras, confined-space, and underwater capture in a single mobilisation. You do not need five providers for five environments. One team documents the complete picture regardless of access constraints.

Measurement-grade processing: Sub-centimetre georeferenced outputs with full metadata chains. Not just photos. Calibrated measurements, defect identification, severity grading, and condition. Evidence that holds up in litigation, satisfies reinsurers, and eliminates disputes.

Enterprise digital twin platform: Your adjusters, underwriters, and claims managers access interactive 3D models through a standard web browser. No specialist software. No IT integration to start. Navigate any property, indoors and exterior, take measurements, visualise digital surface models, annotate damage, and compare pre- and post-conditions and other trends over time. The platform scales across your entire portfolio.

Scalable network: Variable demand is the reality of insurance. Three properties this week, three hundred next week, after a cyclone. A structured program gives you surge capacity without fixed headcount. Scale up for events, scale down between them. No idle capacity cost.

Analyst capability: Condition reports, not data dumps. Professional assessment of what the evidence shows, delivered in formats your teams can action immediately and categorised to align with your systems and processes. The difference between receiving 500 photos and receiving a prioritised assessment with severity grading, geotagged, a visual interactive model and recommended actions.

See What a Structured Assessment Program Looks Like

What Your Adjusters Actually Receive

Every engagement produces measurement-grade deliverables accessible via browser. No specialist software required.

Sub-centimetre aerial capture with AI defect overlay

Roof Condition Orthomosaic

Sub-centimetre resolution aerial capture processed into a georeferenced, measurable map. AI defect detection identifies cracks, membrane failures, ponding, and debris. Every pixel is GPS-located and timestamped.

RGB + Thermal comparison revealing hidden moisture

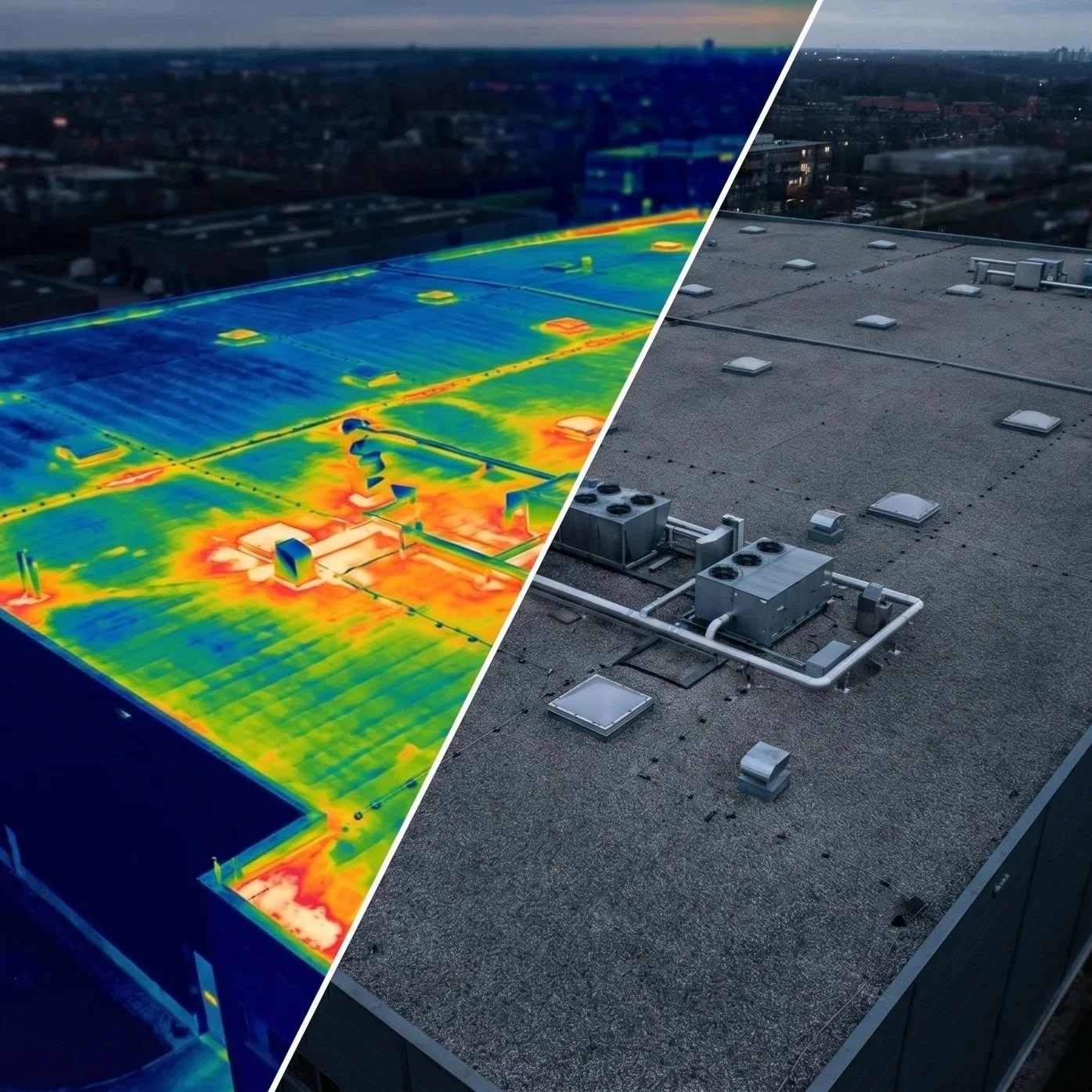

Concealed Defect Detection

Calibrated radiometric thermal imaging reveals moisture ingress, insulation failures, electrical hotspots, and leak paths invisible to standard photography. Temperature accurate to plus or minus 2 degrees Celsius.

Interactive 3D viewer with annotations and measurements

Interactive 3D Digital Twin

Browser-based 3D model accessible to all authorised parties. Navigate, measure, annotate, and compare pre-loss and post-loss conditions. Multiple adjusters work simultaneously from the same dataset. No software installation required.

Pre-loss baseline vs post-event measurement overlay

Pre-Loss vs Post-Loss Comparison

Measurement-grade overlay showing exactly what changed, when, and by how much. Eliminates disputes about pre-existing conditions. Quantifies damage for accurate scoping. Proves causation for subrogation recovery.

Frequently Asked Questions

For declared catastrophe events, mobilisation begins within 24-48 hours. Area-wide aerial capture documents entire affected zones in a single deployment, creating a georeferenced dataset that multiple desk-based adjusters can access simultaneously. After the 2024 Calgary hailstorm (130,000+ claims), drone-assisted teams completed nearly 1,000 property inspections in five weeks at 6-13 minutes per property. Ground-level, interior, and underwater capture can be integrated into the same mobilisation where required.

A pre-loss digital twin creates a timestamped, measurement-grade record of property condition before any event occurs. When a claim is lodged, adjusters compare the pre-loss baseline against post-event capture to objectively determine what damage is new versus pre-existing. This eliminates the subjective judgment that creates disputes and closes the opportunity for fraudulent claims. The Insurance Fraud Bureau of Australia estimates $2.2 billion in fraudulent claims annually, with 75% going undetected. Objective pre-loss evidence removes the ambiguity that fraud relies on.

Published case studies demonstrate measurable returns: 30% reduction in loss adjustment expense (Bees360/AWS), 37% faster settlement with carriers (Master Restoration/Matterport, 2024), and 3.5 workdays saved per claim through remote assessment alone (ATI Restoration/Matterport, 2021). For batch property assessments starting from $250 per property versus $500-$1,500+ for traditional individual site visits, the cost per assessment drops further at program scale. The primary ROI drivers are reduced site visits, faster cycle times, fewer disputed claims, and lower fraud exposure.

Yes. Data captured using calibrated, enterprise-grade sensors with full metadata chains (GPS coordinates, timestamps, sensor calibration certificates, operator credentials) meets the evidentiary standards required by Australian courts. When captured under an ISO 9001 quality management system with documented chain of custody, this evidence is used in engineering expert reports, insurance litigation, subrogation claims, and dispute resolution proceedings. All deliverables include methodology statements suitable for expert report annexures.

Yes. Interactive 3D models, high-resolution imagery, thermal overlays, and measurement tools are accessed through a standard web browser. No specialist software installation or IT integration is required to begin. Adjusters navigate to any property in the dataset, take measurements, annotate damage, compare pre-loss and post-loss conditions, and complete assessments remotely. Multiple adjusters can work simultaneously across the same dataset, which is how one capture supports hundreds of remote assessments.

The program covers all property types and access environments in a single provider relationship: residential (batch roof assessment), high-rise and strata (facade, balconies, plant rooms), commercial (roof condition, renewal inspections), industrial (complex structures, hazardous environments), agricultural and rural (large-area mapping), marine and waterfront (hull, marina, submerged infrastructure via ROV), and land or broadacre (flood extent, erosion, boundary disputes). Aerial, ground-level 360, confined space, thermal, and underwater capture are combined as needed per property.

Calibrated radiometric thermal sensors detect conditions invisible to standard photography: moisture ingress beneath roof membranes, electrical hotspots indicating fire risk, insulation failures, HVAC leaks, and concealed water damage. Temperature measurements are accurate to plus or minus 2 degrees Celsius. For underwriting, thermal data identifies risks that would otherwise go undetected until they become claims. For claims, thermal evidence establishes causation chains for subrogation by demonstrating that specific defects existed prior to loss events.

Insurance demand is inherently variable. Three properties this week, three hundred next week after a cyclone. A structured program provides surge capacity without fixed headcount. The operator network scales up for catastrophe events and scales down between them, so you are not carrying idle capacity cost. During quiet periods, the program focuses on annual baseline captures, renewal inspections, and portfolio condition monitoring. During events, the same infrastructure pivots to rapid area-wide response with priority mobilisation for program clients.

Individual property assessments start from $250 per property for image capture and batch assessment, with condition reports and 3D models priced on scope. Area-wide catastrophe capture is priced per deployment based on the geographic area and number of properties within the zone. Annual baseline programs are priced per property per capture cycle with volume pricing applied at scale. Program clients receive priority CAT response guarantees as part of their retainer. The cost per assessment drops significantly at program scale compared to traditional individual site visits at $500-$1,500+ each. A scoping discussion defines exact deliverables and pricing structure for your portfolio.

All deliverables are produced in industry-standard formats compatible with existing claims workflows. High-resolution imagery, measurements, and condition reports can be attached directly to claim files within Xactimate, Symbility, ClaimCenter, and other platforms your team already uses. Interactive 3D models are accessed via browser link, requiring no software installation or IT integration. Georeferenced orthomosaics export as GeoTIFF for GIS systems. Measurement data exports in formats that align with Xactimate sketch and measurement tools, allowing estimators to pull verified dimensions directly into their scope of works rather than relying on manual field measurements. We work with your operations team during onboarding to align output formats with your specific system requirements.

We operate Australia-wide from our Gold Coast headquarters, with engagements scoped nationally and internationally. For catastrophe events, our scalable operator network deploys to any affected region within 24-48 hours regardless of location. For annual baseline programs, capture schedules are planned around your portfolio geography with local operators coordinated through our quality management system. CASA certification, $20M public liability insurance, and ISO-certified management systems apply to all engagements regardless of location.

Integrated Services

Digital Twin and 3D Modelling

Create exact, interactive digital replicas of assets & incident sites for immersive insights, presentations and remote loss adjustment

Aerial Inspection and Capture

Rapid, 360 degree high-resolution documentation of condition, damage or claim following natural disasters or asset failures.

Thermal and Condition Assessment

Detect hidden moisture intrusion, electrical faults, and structural anomalies critical to determining the root cause of a loss.

Underwater Asset Inspection & Condition Intelligence

Secure vital information from above and below the surface, from submerged infrastructure, marine vessels, ports, marinas and flooded environments safely and efficiently.